wealth management has carried a reputation of exclusivity a financial service meant only for high-net-worth individuals, executives, or the ultra-wealthy. When most people hear the term, they picture private bankers, million-dollar portfolios, and luxury financial planning services out of reach for the average person. But is that image accurate? Is wealth management truly only for the rich or is it something that everyday people can benefit from

Key Takeaways

- Wealth management is about organizing, growing, and protecting your money.

- It’s not exclusive to the rich — it’s for anyone who wants to take control of their financial future.

- Today’s tools make wealth planning accessible and affordable to all.

- Start small, be consistent, and grow your knowledge over time.

- Building wealth is not about luck — it’s about planning, discipline, and time.

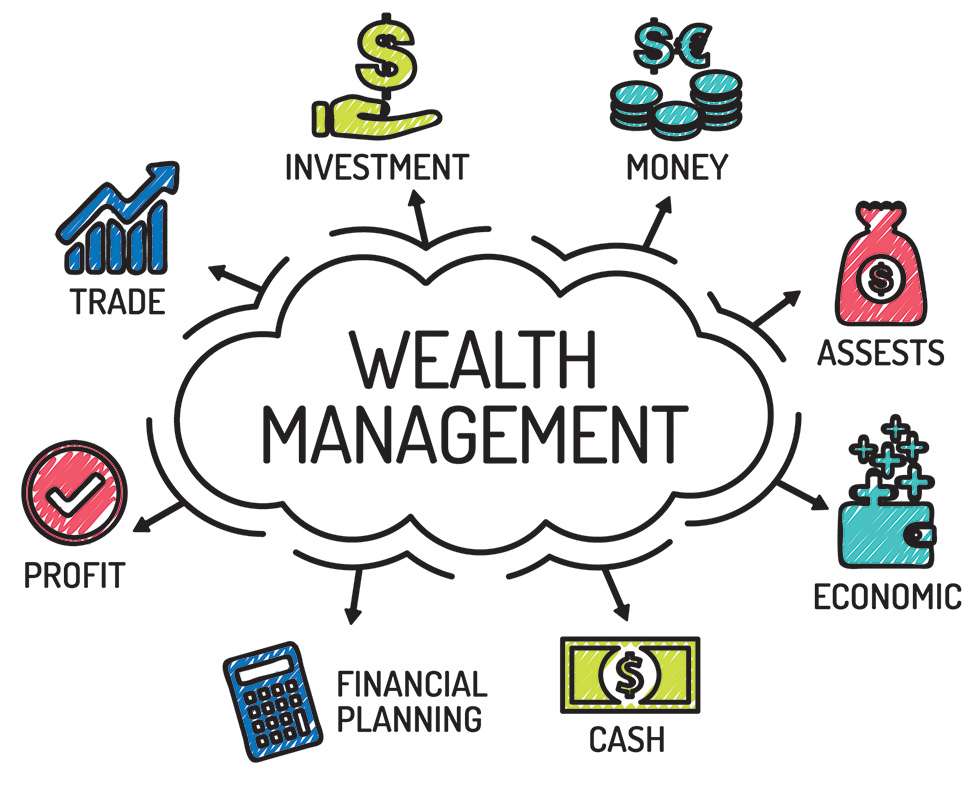

What Is Wealth Management?

Wealth management is a comprehensive approach to managing your financial life. It integrates investment management, financial planning, retirement preparation, tax strategies, insurance, and estate planning — all designed to grow and protect your wealth over time.

Key Services Often Included:

Absolutely! Here’s a more detailed breakdown of each core component of wealth management. These are the essential services that can benefit individuals at any stage of financial life — not just the wealthy:

Investment Advice and Portfolio Management

Investment advice is at the heart of wealth management. It involves building a customized investment strategy based on your financial goals, risk tolerance, and time horizon. Key components include:

- Asset Allocation: Spreading investments across stocks, bonds, real estate, and alternative assets to balance risk and return.

- Diversification: Reducing exposure to any single investment or sector to protect against losses.

- Rebalancing: Periodically adjusting your portfolio to maintain your desired asset mix.

- Performance Monitoring: Tracking how your investments perform and making changes as needed.

Even small portfolios can benefit from guidance to avoid common mistakes and make informed decisions.

Tax Planning and Optimization

Wealth management isn’t just about growing money — it’s also about keeping more of what you earn. Tax planning focuses on legally minimizing your tax liability:

- Tax-Deferred Accounts: Using accounts like IRAs and 401(k)s to delay taxes on investments.

- Tax-Efficient Investments: Choosing ETFs or index funds to reduce capital gains taxes.

- Tax-Loss Harvesting: Selling losing investments to offset gains and reduce tax bills.

- Income Strategy: Managing when and how to withdraw income in retirement to minimize tax burdens.

Effective tax planning can add significant value to your long-term wealth strategy.

Retirement Planning

Planning for retirement means ensuring you’ll have enough money to maintain your lifestyle after you stop working. Wealth managers help clients:

- Estimate Retirement Needs: Assessing how much you’ll need based on inflation, life expectancy, and lifestyle.

- Choose Retirement Vehicles: IRAs, 401(k)s, Roth accounts, annuities, etc.

- Contribution Strategies: How much to save and where to invest it.

- Withdrawal Planning: Managing drawdowns and Required Minimum Distributions (RMDs) to maximize tax efficiency and income.

- Social Security Planning: Determining the best time to start benefits.

Starting early — even with small amounts — can make a major difference thanks to compound growth.

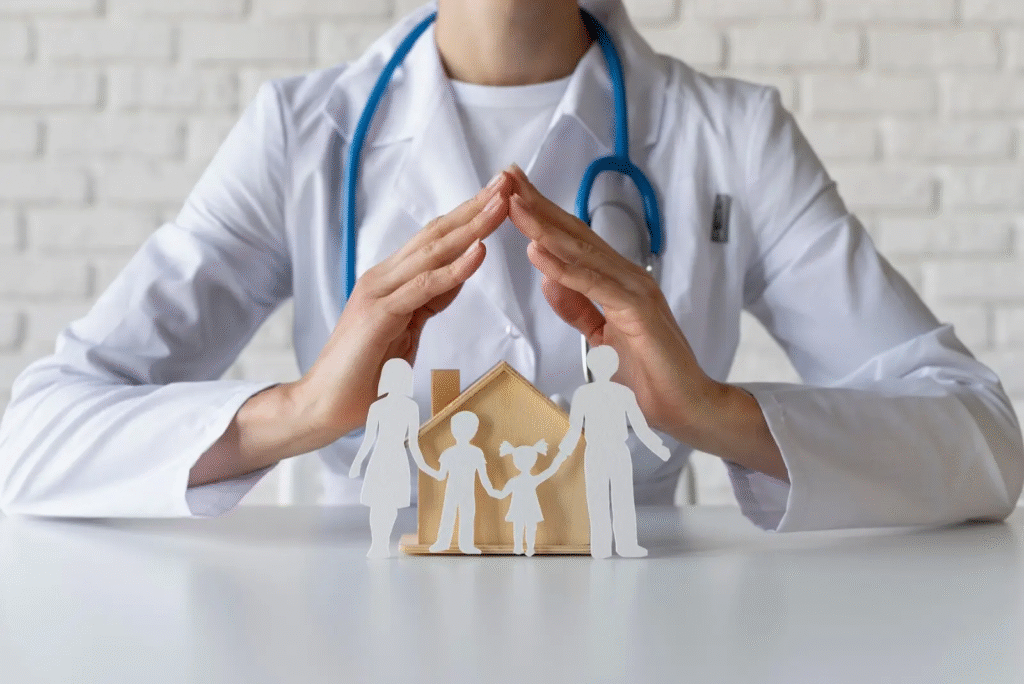

Insurance Analysis

Insurance is a key part of risk management and wealth preservation. Wealth managers assess and recommend coverage in areas such as:

Life Insurance

Life insurance provides a financial safety net for your family or dependents in the event of your death. It can cover funeral costs, replace lost income, and help pay off debts like mortgages or loans.

Health Insurance

Health insurance helps cover the cost of medical care, including doctor visits, hospital stays, surgeries, and prescription drugs. It protects you from the financial burden of unexpected illnesses or accidents.

Disability Insurance

Disability insurance replaces a portion of your income if you become unable to work due to illness or injury. It ensures that you can maintain your lifestyle and meet financial obligations even without a paycheck.

Property and Liability Insurance

This type of insurance protects your physical assets — like your home, car, or personal belongings — from damage or theft. Liability coverage shields you from legal or financial responsibility if someone is injured on your property.

Long-Term Care Insurance

Long-term care insurance helps cover the cost of services like nursing homes, assisted living, or in-home care when you’re older or unable to perform daily activities. It prevents retirement savings from being drained by extended care needs.

Many people are either underinsured or overpaying — a wealth manager ensures your protection is aligned with your financial plan.

Estate Planning (Wills, Trusts, etc.)

Estate planning ensures your assets are distributed according to your wishes and minimizes the legal and tax burden for your heirs.

Wills

A will is a legal document that outlines your wishes for how your property, finances, and personal belongings should be distributed after your death. It also allows you to name guardians for minor children and specify funeral preferences. Without a will, state laws determine how your estate is divided, which may not reflect your intentions. A will can help prevent family disputes and ensure your legacy is handled properly.

Trusts

Trusts are legal arrangements that allow a third party, or trustee, to hold and manage assets on behalf of beneficiaries. Trusts can bypass probate, offer tax benefits, and provide more control over when and how assets are distributed. They are useful for protecting wealth, ensuring privacy, and managing complex family or financial situations. Trusts can be revocable (modifiable) or irrevocable (fixed).

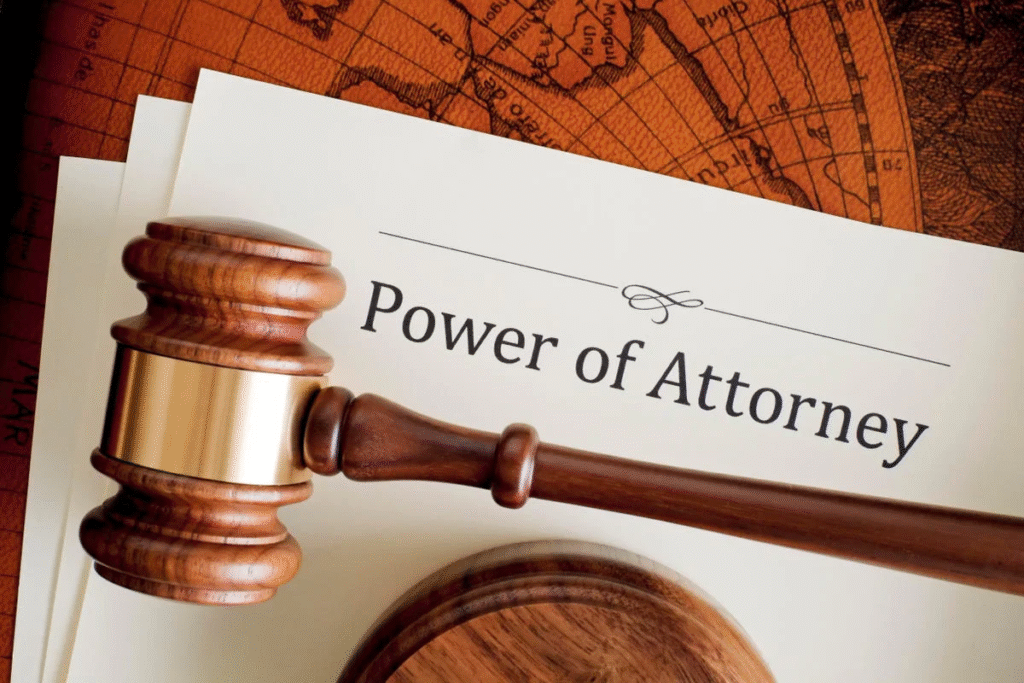

Power of Attorney (POA)

A Power of Attorney grants a trusted individual the legal right to act on your behalf in financial, legal, or medical matters if you become incapacitated. There are different types (general, durable, medical) depending on the authority you wish to delegate. Having a POA ensures that important decisions can be made promptly and according to your wishes when you are unable to act for yourself.

Healthcare Directives (Living Will)

A healthcare directive, or living will, specifies your preferences for medical treatment if you are unconscious or otherwise unable to communicate. This includes decisions about life support, resuscitation, and organ donation. It helps relieve family members from having to make difficult choices under stress and ensures your medical care aligns with your values and beliefs.

Beneficiary Designations

Beneficiary designations determine who receives assets from life insurance policies, retirement accounts (like IRAs or 401(k)s), and some bank accounts when you pass away. These designations override your will, so they must be reviewed regularly to reflect life changes like marriage, divorce, or births. Keeping them updated ensures your assets go to the intended individuals quickly and without legal disputes.

Estate planning isn’t just for the ultra-wealthy — anyone with dependents, property, or savings should have a plan in place.

Budgeting and Debt Reduction

Wealth management starts with the basics: knowing where your money goes and managing it wisely.

- Creating a Budget: Planning and tracking income and expenses to maximize savings.

- Debt Analysis: Understanding all forms of debt — credit cards, student loans, mortgages.

- Debt Repayment Strategies: Using methods like the snowball or avalanche approach to reduce liabilities.

- Cash Flow Management: Ensuring there’s always enough to cover expenses and fund goals.

This is often the first step in financial stability — and one that many overlook or underestimate.

Risk Management

Risk is an unavoidable part of life and investing, but it can be managed. Wealth managers help:

- Identify Financial Risks: Loss of income, market downturns, unexpected health issues.

- Mitigate Risks Through Diversification: In both investments and income sources.

- Apply Insurance Strategically: To transfer financial risk to insurers.

- Plan for Emergencies: With sufficient cash reserves and contingency plans.

The Myth: Wealth Management Is Only for the Rich

Why People Think That:

- Many traditional wealth managers only take clients with assets over $500,000 or $1 million.

- Wealth management firms often market to high-net-worth individuals (HNWIs).

- There’s a stigma that financial advisors are expensive or “only for the elite.”

The Truth:

- Today, many firms offer scaled-down or digital versions of wealth management (robo-advisors, financial coaching).

- The core principles of wealth management — saving, investing, tax planning — are beneficial at all income levels.

- You don’t need millions to benefit from planning for your future.

Why Wealth Management Is for Everyone

Helps You Grow Wealth — No Matter Your Starting Point

Even small consistent efforts in investing and saving can compound into significant results over time.

Protects Against Financial Shocks

Wealth management includes insurance and emergency fund planning — critical for people of any income level.

Aligns Finances with Goals

Whether you want to buy a home, pay off debt, or retire early, a wealth management approach helps you stay organized and strategic.

Improves Financial Literacy

You learn how to use financial tools, track net worth, invest wisely, and understand how taxes and debt work.

Tools and Strategies Accessible to Everyone

| Tool | Description | Who It’s For |

|---|---|---|

| Budgeting apps | Helps track spending/saving | Everyone |

| Robo-advisors | Low-fee automated investing | Beginners |

| ETFs & Index Funds | Low-cost diversified investments | Investors with any budget |

| Emergency Fund | 3–6 months of expenses | Everyone |

| Term Life Insurance | Affordable protection for dependents | Families |

| Roth IRA/401(k) | Tax-advantaged retirement savings | All income levels |

| Fee-only financial advisors | Pay only for advice, not commissions | Budget-conscious planners |

Tiered Wealth Management: From Basic to Advanced

Basic (Beginner – Low Income):

- Budgeting

- Emergency fund

- Paying off debt

- Using robo-advisors

- Retirement account contributions (even small ones)

Intermediate (Growing Income):

- Diversified investments (ETFs, mutual funds)

- Tax planning

- Saving for a home, education

- Disability and life insurance

Advanced (High Income or Business Owner):

Estate and Legacy Planning

Estate and legacy planning involves organizing your assets and wishes to ensure a smooth transfer of wealth to your heirs while minimizing taxes and legal complications. It focuses on preserving your legacy and supporting future generations according to your values.

Tax-Loss Harvesting

Tax-loss harvesting is a strategy where you sell investments at a loss to offset capital gains taxes on other investments. This helps reduce your overall tax liability while maintaining your portfolio’s asset allocation.

Charitable Giving Strategy

A charitable giving strategy allows you to support causes you care about while gaining potential tax benefits. It can include direct donations, donor-advised funds, or planned giving through trusts and bequests.

Trusts and Wealth Transfe

Trusts are legal tools used to transfer wealth efficiently while protecting assets from probate and potentially reducing estate taxes. They allow you to control how and when your beneficiaries receive their inheritance.

Business Succession Planning

Business succession planning prepares for the transfer of ownership and management of a business to the next generation or new owners. It ensures continuity, minimizes disruption, and protects the value of the business.

How to Start Wealth Management at Any Income Level

- Track every dollar – Use a simple app or spreadsheet

- Set clear financial goals – Short, medium, and long-term

- Start small investments – Even $50/month can grow

- Create an emergency fund – Avoid financial derailments

- Use retirement accounts – 401(k), IRA, Roth IRA

- Seek free or affordable advice – Online communities, fee-only planners, financial Literacy courses

Also Read: What Is Financial Planning And Why Is It So Important?

Conclusion

Wealth management is no longer a service exclusive to the rich—it is an essential tool for anyone seeking financial security and growth. By adopting smart strategies, regardless of income level, individuals can protect their assets, plan for the future, and build lasting wealth. Starting early and staying disciplined makes wealth management accessible and valuable for everyone.

Wealth management isn’t just for the rich — it’s a mindset and strategy that benefits everyone. Whether you’re earning $30,000 or $300,000, managing your money wisely can help you:

- Achieve life goals

- Gain peace of mind

- Prepare for emergencies

- Build long-term security

You don’t need to wait until you’re wealthy to start managing wealth — you become wealthy by starting to manage your money now

FAQs

Do I need a financial advisor to do wealth management?

Not necessarily. Many tools (apps, robo-advisors) are available. Advisors help with personalized strategies but aren’t required.

What’s the difference between financial planning and wealth management?

Financial planning focuses on goals and budgeting. Wealth management is broader — covering investment, tax, estate, and risk strategies.

Is wealth management worth it if I’m in debt?

Yes. Managing wealth includes getting out of debt, building savings, and avoiding financial pitfalls.

What income level is ideal for starting wealth management?

There’s no minimum. It’s more about your mindset and willingness to take control of your finances.

Are robo-advisors effective?

Yes, especially for beginners. They offer diversified portfolios, automated rebalancing, and low fees.

Can I do wealth management on my own?

Yes, with the right education and discipline, you can manage your own wealth. Many people start with online resources, budgeting tools, and investment platforms to take control of their finances.

How often should I review my wealth management plan?

At least once a year, or when you experience major life changes (like marriage, a new job, or having a child). Regular reviews help ensure your plan stays aligned with your goals.